The appeal of Pay Later services lies in their ability to eliminate the need for credit cards, provide instant approval, and offer flexibility in repayment.

India’s digital payment landscape has undergone a remarkable transformation over the past decade, with the Unified Payments Interface (UPI) playing a pivotal role. A recent AT Kearney report reveals a clear shift towards digital payments, with 90% of consumers preferring them for online purchases and 50% for offline transactions. This trend is particularly evident in discretionary purchases, where over 85% of respondents favour digital payment methods.

The widespread adoption of UPI has been a game-changer, gaining acceptance across diverse geographic and income segments. Digital payments now account for 65% of transactions in smaller towns and 75% in larger cities, signifying broad nationwide adoption. However, despite UPI’s dominance, credit cards continue to hold sway over high-value purchases, thanks to their greater purchasing power and attractive perks such as cashback and rewards.

The Credit Gap and the Pay Later Opportunity

With only around 102 million credit cards in circulation, India’s credit penetration remains relatively low. This presents a significant opportunity, especially considering the country’s burgeoning middle class of approximately 432 million consumers with household incomes ranging between ₹500,000 and ₹3,000,000 annually.

Enter Pay Later services, which have rapidly gained popularity by offering near-instant approval, flexibility, and access to credit without the need for traditional credit cards. These services have found resonance among younger, tech-savvy consumers. In India’s top six metros, 40% of consumers have already embraced Pay Later services, while smaller cities and towns present a ripe market for expansion.

The appeal of Pay Later services lies in their ability to eliminate the need for credit cards, provide instant approval, and offer flexibility in repayment. This model has enabled fintech companies and NBFCs to establish strong relationships with retailers and consumers by embedding credit directly into the checkout process, driving higher conversion rates and increased spending.

UPI-Linked Credit: The Next Frontier

As UPI has already transformed payment habits in India, the natural evolution lies in UPI-linked Pay Later options. These services allow consumers to access pre-approved credit lines directly through their UPI apps, offering unparalleled convenience. Specifically designed to serve customers with loan requirements up to ₹50,000, UPI-linked credit lines provide a low-cost, accessible alternative to traditional credit cards.

This solution is particularly promising given the low penetration of credit cards—only 10% of consumers currently own a credit card in India. With the vast middle class eager for flexible financing options, UPI-linked credit products present a massive untapped market for banks.

How Can Banks Monetise the Pay Later Market

Banks are uniquely positioned to dominate the Pay Later market, leveraging their existing infrastructure, customer trust, and advanced financial capabilities to offer seamless Pay Later services within their existing apps, such as UPI or Banking SuperApps. This integration enables a frictionless experience for users already engaged with their digital platforms.

Moreover, banks have a distinct advantage in extending responsible, tailored credit to their customers, thanks to their access to detailed customer data. This enables them to reduce the risk of defaults and offer flexible repayment plans that cater to individual needs. By partnering with merchants for point-of-sale integration and implementing advanced risk and fraud management tools, banks can ensure sustainable and scalable Pay Later services.

The National Payments Corporation of India’s (NPCI) guidelines, effective from October 16, 2024, also present a lucrative opportunity for banks. An interchange fee of 1.2% will be charged on transactions made via pre-approved UPI credit lines, providing a new revenue stream for banks offering these services. Furthermore, UPI-linked credit offers banks a chance to tap into new customer segments that are underserved by traditional credit products. With lower fees compared to traditional credit cards, UPI-linked credit is poised to attract more merchants, driving higher adoption rates. Banks can also generate additional income from late payment interest fees, further expanding their revenue streams. By embracing UPI-linked credit, banks can expand their offerings, tap into a broader market, and solidify their position in the Pay Later space.

The Way Forward

As the Pay Later market continues to evolve, banks must act swiftly to claim their stake. By leveraging UPI-linked credit solutions, they can tap into this fast-growing market while promoting financial inclusion and offering consumers greater purchasing power.

The integration of UPI-linked credit represents a significant step forward in India’s digital payment ecosystem. It offers a flexible, convenient solution for consumers while unlocking new revenue streams for banks. As this technology continues to develop and gain widespread adoption, it has the potential to reshape the landscape of consumer credit in India, bridging the gap between traditional banking services and the needs of the modern, digitally savvy consumer.

Explore More

November 12, 2024

Media Buzz,

India’s QR soundbox boom: how acquirers can ride the offline payment wave

Read More

October 23, 2024

Media Buzz,

Transforming Financial Inclusion: Bringing 800 Million More Indians into the UPI Circle

Read More

October 18, 2024

Newsroom,

NPST Achieves 264% Growth in Q2 FY’25 Net Profit, Announces Move to Mainboard

Read More

October 17, 2024

Media Buzz,

The Consumer-Centric Evolution: Banks Must Modernizing UPI Switches Before It’s Too Late

Read More

October 8, 2024

Media Buzz,

UPI Circle: The big-bank opportunity to bridge India’s financial gap

Read More

September 24, 2024

Newsroom,

NPST Launches Seven AI-Powered Digital Payment Products at Global Fintech Fest 2024

Read More

September 5, 2024

Newsroom,

UPI: The world’s favourite payment method hits $964 billion in record time

Read More

September 4, 2024

Newsroom,

What's the true value that delegated payments through UPI Circle delivers to banks and customers

Read More

July 23, 2024

Newsroom,

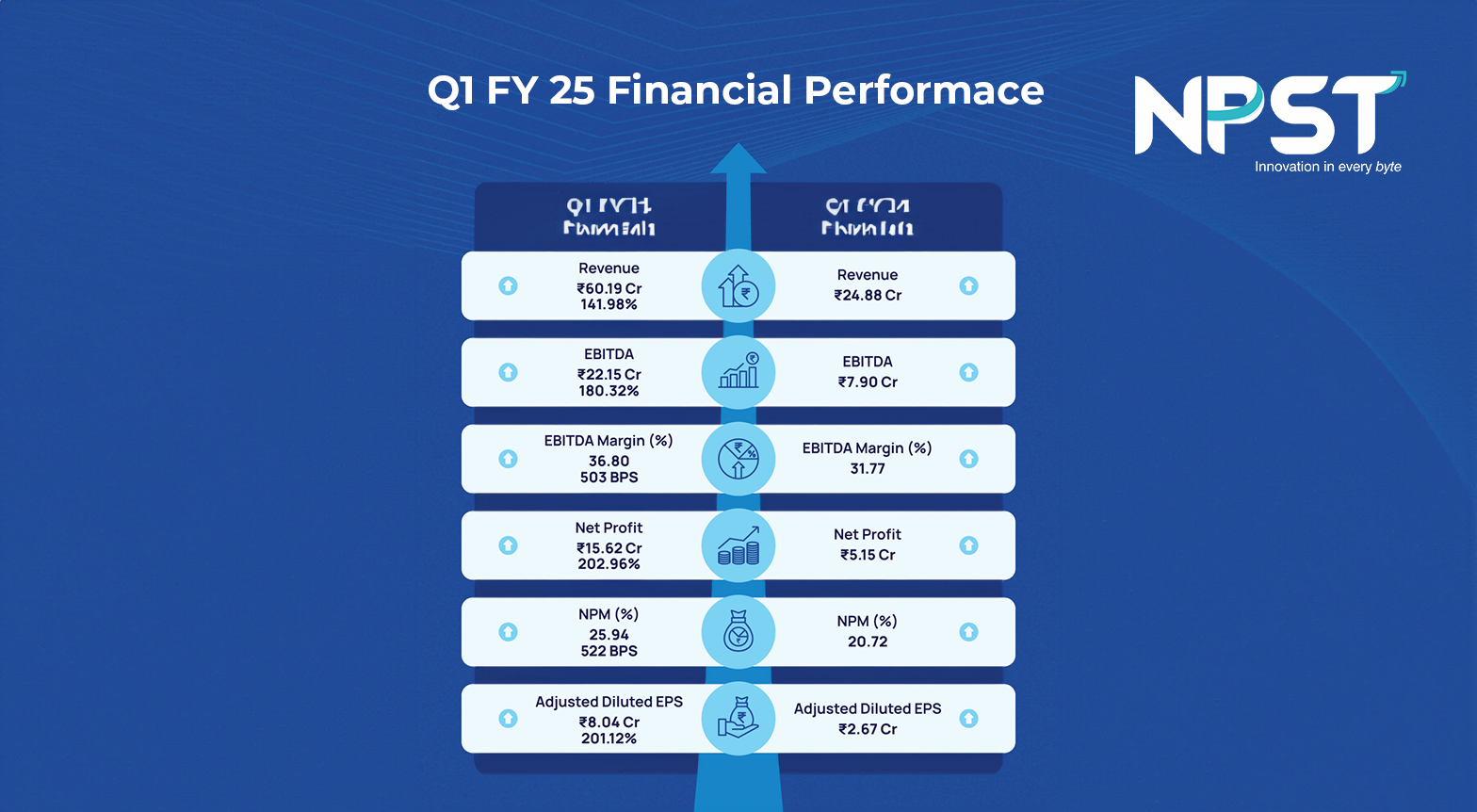

NPST Q1 FY 25 Results: Net Profit Surges by 202%, Marking Best-Ever Quarterly Performance

Read More

We empower banks and payment aggregators to achieve success at every step of the transaction journey