In today’s fast-paced digital landscape, the mantra for banks should be straightforward: “Consumer, Consumer, and only Consumer.” Nowhere is this more evident than in the unprecedented success of the Unified Payments Interface (UPI) across India. What began as a simple platform for real-time account-to-account transfers has evolved into an integral part of India’s payment ecosystem, extending to prepaid cards, credit cards, wallets, and mandates.

Today, UPI dominates digital payments, accounting for over 90% of transactions across urban and rural regions alike. This transformation reflects a clear shift toward consumer-centric innovation, making UPI indispensable for person-to-merchant (P2M) transactions, the driving force behind India’s payments revolution. While this shift toward consumer convenience and innovation is undoubtedly positive, it has also exposed a significant gap in the banking sector’s back-end infrastructure.

The Challenges of Legacy Infrastructure

Despite the introduction of cutting-edge UPI-driven services, many banks still rely on first-generation UPI switches — systems that are often over a decade old. These legacy systems, once groundbreaking, are now struggling to keep pace with the increasing demands of modern banking. This results in slower transaction processing, frequent system outages, and an inability to scale efficiently.

1. Limited Scalability: One of the most pressing issues banks face is the limited scalability of outdated UPI systems. In September 2024 alone, UPI processed over 15 billion transactions, averaging more than 500 million transactions daily. With such high transaction volumes, legacy systems frequently experience downtime, negatively impacting consumer experience and tarnishing the bank’s reputation.

2. Integration to Innovation: Many first-generation UPI switches require anywhere from 12 to 18 weeks to integrate new features, leading to missed opportunities and stagnation. On the other hand, UPI has expanded to support a variety of channels — prepaid cards, wallets, mandates, and even IoT-enabled payment devices like connected cars and smartwatches. However, incorporating these services into outdated systems is complex as legacy switches weren’t built to accommodate such advancements. This makes it harder for banks to keep up with evolving consumer demands.

3. Elevated Operational Expenses: Maintaining first-generation UPI switches is not only inefficient but costly. The resources allocated to maintaining these aging systems divert funds from innovation initiatives that could enhance customer experiences. This “technical debt” is compounded over time, requiring more investment to keep systems running smoothly while stifling progress.

4. Risk Exposure: Sophisticated fraud threats are on the rise, and many legacy UPI switches simply cannot support the advanced fraud prevention mechanisms required to protect consumers. As regulatory pressures mount and customer expectations for secure transactions increase, banks can no longer afford to operate with systems that leave them vulnerable to cyberattacks and fraud.

5. Regulatory Compliance and System Resilience: Beyond technical issues, banks must also contend with increased regulatory scrutiny. While international frameworks like the European Union’s Digital Operational Resilience Act (DORA) do not directly apply in India, the emphasis on resilience and system security is becoming a global trend. In India, regulators are mandating stricter reporting of system outages and compliance with evolving digital standards. Banks relying on legacy infrastructure will find it increasingly difficult to meet these stringent requirements, exposing them to regulatory risks and penalties.

The Path Forward for Modernisation

For banks looking to modernize their UPI infrastructure, the idea of a complete system overhaul can seem overwhelming. However, a more agile and practical solution lies in adopting a multi-switch model. This approach allows banks to implement next-generation UPI switches alongside their existing systems, enabling incremental scaling and increased flexibility in a fast-changing payment ecosystem.

Banks may embrace a modular architecture with plug-and-play features, to tailor their infrastructure to meet specific business needs. For example, small finance banks might focus on switches dedicated to managing credit lines, while payment banks could prioritize systems optimized for wallet transactions. These targeted, modular upgrades allow for continuous innovation without sacrificing operational stability.

They also consider microservices to enhance this flexibility to deploy independent and scalable services based on demands. Coupled with technologies like containerization and NoSQL databases, these systems can significantly boost performance, particularly in handling high-volume, real-time transactions. This modern architecture ensures that banks remain agile while offering the speed and reliability that customers expect.

On the security front, next-generation UPI switches come equipped with advanced features such as encryption, tokenization, and real-time fraud detection. These security measures not only protect consumer data but also help banks comply with increasingly stringent regulatory standards, all without compromising transaction speed or efficiency.

As the digital payments landscape continues to evolve, banks must recognize that standing still is not an option. Outdated infrastructure hampers innovation and threatens both customer satisfaction and revenue. By adopting modern, flexible payment systems, banks can stay ahead of the curve and offer the seamless, secure, and scalable experiences today’s consumers’ demand. The future of banking hinges on adaptability, and the time for modernization is now.

Explore More

November 12, 2024

Media Buzz,

India’s QR soundbox boom: how acquirers can ride the offline payment wave

Read More

October 23, 2024

Media Buzz,

Transforming Financial Inclusion: Bringing 800 Million More Indians into the UPI Circle

Read More

October 18, 2024

Newsroom,

NPST Achieves 264% Growth in Q2 FY’25 Net Profit, Announces Move to Mainboard

Read More

October 8, 2024

Media Buzz,

UPI Circle: The big-bank opportunity to bridge India’s financial gap

Read More

September 24, 2024

Newsroom,

NPST Launches Seven AI-Powered Digital Payment Products at Global Fintech Fest 2024

Read More

September 5, 2024

Newsroom,

UPI: The world’s favourite payment method hits $964 billion in record time

Read More

September 4, 2024

Newsroom,

What's the true value that delegated payments through UPI Circle delivers to banks and customers

Read More

July 23, 2024

Newsroom,

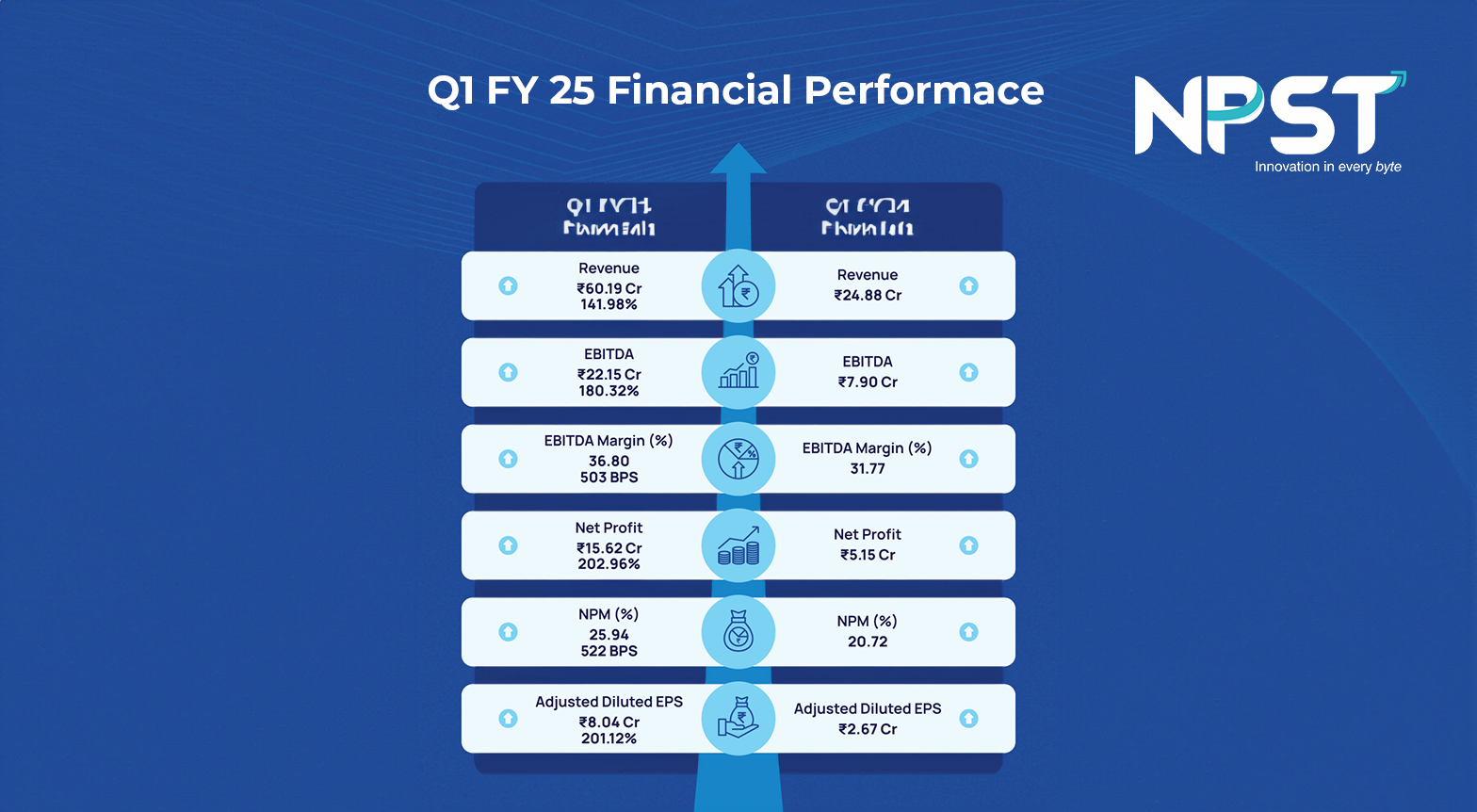

NPST Q1 FY 25 Results: Net Profit Surges by 202%, Marking Best-Ever Quarterly Performance

Read More

We empower banks and payment aggregators to achieve success at every step of the transaction journey